Your credit score might just be a three-digit number, but it carries a lot of weight in your financial life. A low credit score can close doors to many opportunities—loans, credit cards, mortgages, and more. Beyond borrowing, it can even affect your ability to rent an apartment, land a job, or get affordable insurance.

If you’re facing challenges with a low credit score, exploring personal finance debt relief options can be a helpful step. But first, it’s important to understand exactly what having a low credit score means and how it impacts different parts of your life.

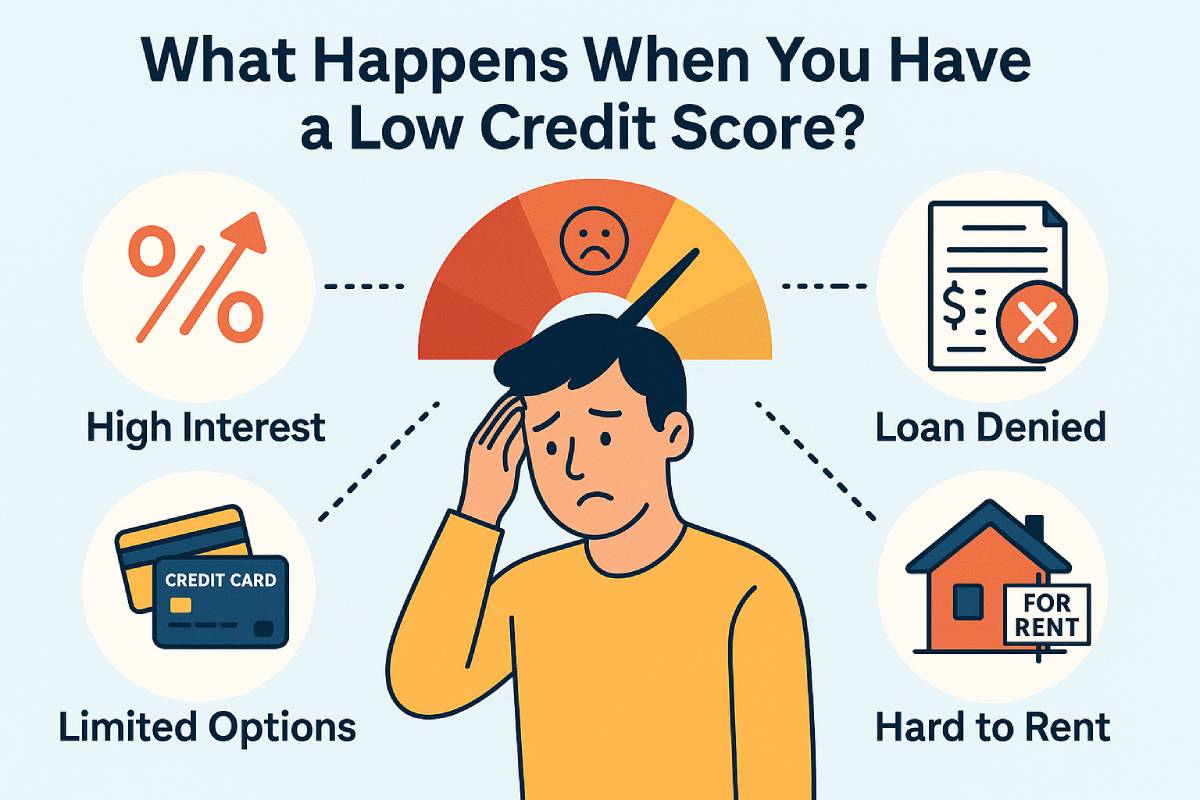

Limited Access to Loans and Credit

One of the most direct effects of a low credit score is difficulty qualifying for loans or credit cards. Lenders view a low score as a sign that you might be a risky borrower. Because of this risk, you might get denied or offered loans with much higher interest rates.

Higher interest rates mean borrowing costs more, which can trap you in a cycle of debt. This makes it harder to pay down existing balances and improve your financial situation.

Challenges in Renting a Home

Landlords often check credit scores as part of the rental application process. A low score can make them hesitate to rent to you, fearing you might miss rent payments or cause financial issues.

This can limit your housing options, making it harder to find a place you want at a price you can afford.

Impact on Employment Opportunities

Many employers check credit reports (though not the score itself) as part of background checks, especially for jobs that involve financial responsibilities. A low score or negative marks on your report could raise concerns about reliability or trustworthiness.

While not all employers use credit checks, it’s an additional hurdle that can make job hunting more challenging.

Higher Insurance Premiums

Insurance companies often use credit-based insurance scores to decide your premiums. A low credit score can result in higher rates for auto or homeowners insurance, costing you more money each month.

Even if you’re financially responsible in other areas, your credit score can still influence these costs.

Emotional and Mental Toll

Beyond financial setbacks, a low credit score can affect your mental and emotional health. Stress, anxiety, and feelings of shame or embarrassment are common.

This emotional toll can make it harder to take positive steps toward improving your finances, creating a difficult cycle to break.

How Personal Finance Debt Relief Can Help

If your low credit score is tied to debt issues, personal finance debt relief programs might provide the support you need. These programs can help negotiate with creditors, reduce payments, and create manageable plans to regain control.

Taking action not only helps your finances but can improve your credit score over time.

Steps to Improve a Low Credit Score

- Pay bills on time: Consistent, timely payments build trust with lenders.

- Reduce credit card balances: Lower utilization helps boost scores.

- Avoid opening too many new accounts: Each application can temporarily lower your score.

- Check your credit report: Dispute errors that unfairly hurt your score.

- Be patient: Improving credit takes time but is achievable with steady habits.

Final Thoughts: A Low Credit Score Isn’t the End

While a low credit score brings challenges, it’s not a permanent label. Understanding its impacts helps you navigate financial hurdles and take steps toward recovery.

Whether through personal finance debt relief or better money habits, rebuilding your credit can open doors to better loans, housing, employment, and peace of mind.

Your score is a snapshot, not your full story—there’s plenty of room to turn things around and build a stronger financial future.

{kind=link}